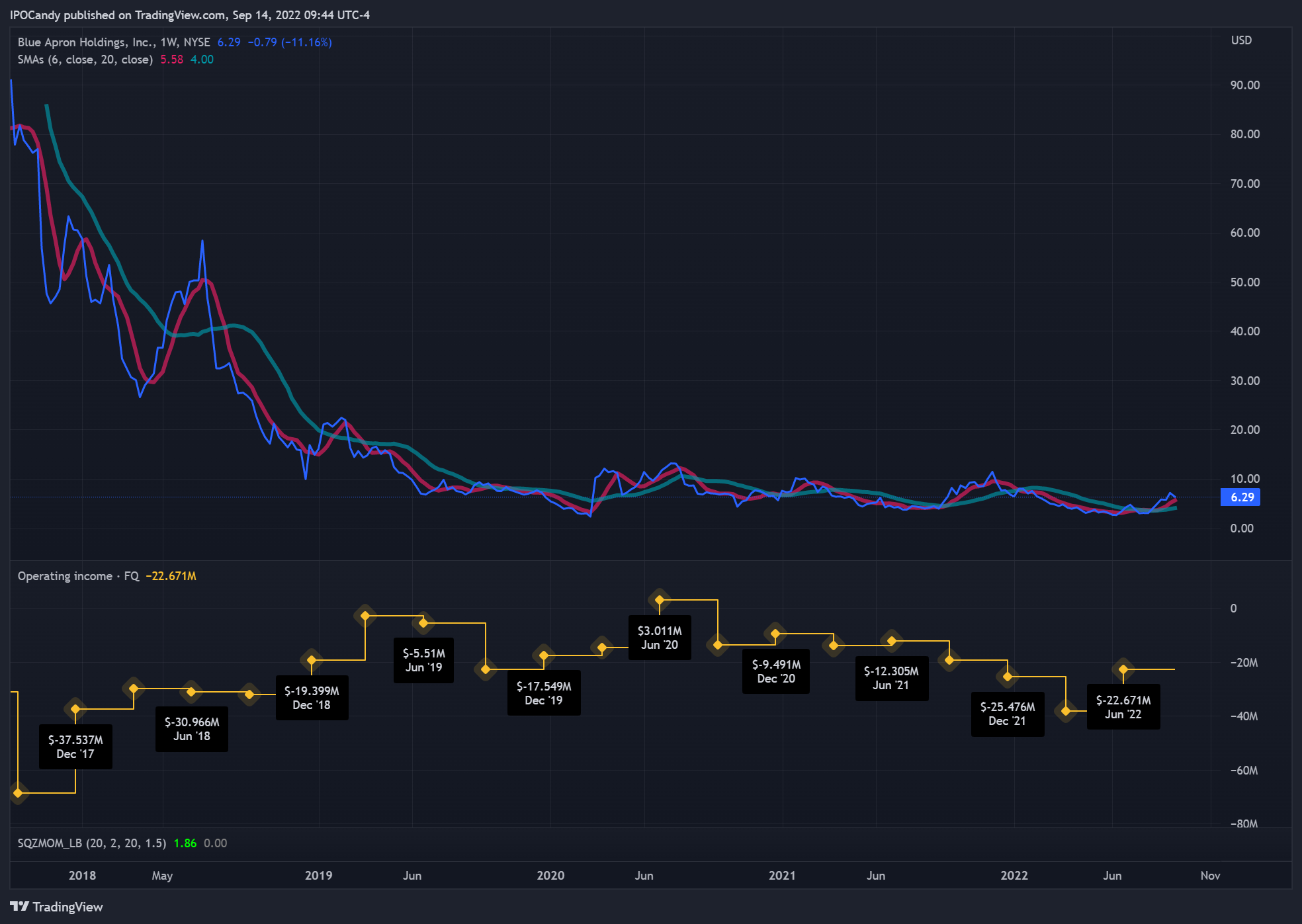

Blue Apron $APRN, the at-home preparation meal service, was a dud of an IPO years ago. In 2017 we published a note entitled "Blue Apron Needs to be Acquired Soon."

My wife and I used the product for a year back when they were still a private company and thought it was good and had a lot of potential for consumers. But management took no initiative to address opportunities to evolve the product to add to its appeal. The meals were good, but they took too much time and effort to prepare. The only time savings was the shopping element.

Why not offer someone pan or oven-ready options? If you get home at 8 pm from a long workday, you might not be in the mood to start chopping vegetables. This is a time many turn to take-out, DoorDash $DASH, etc. But if you had a meal you could put in the oven for 20 minutes while you put on your sweats and picked a show on Netflix $NFLX, that would work just fine. It would offer some healthier options than takeout too.

They also didn't see the opportunity to offer add-ons like entertainment boxes, brunch boxes, baking kits for times when you need to bring something to a bake sale, etc.

Since the IPO, the shares of $APRN look like they have food poisoning.

So Maybe There's a Chance...

The things going for $APRN right now include a cadence of new offerings, a big financing round, high short interest, and tailwinds in the shape of rising DIY cooking costs and skyrocketing eating-out costs. Let's get into those more.

{kind=link}