Skip to content

Dark

Search

Sign In

Subscribe

Home

About

Notes

Decks

SPACs

Spinoffs

AI

Consumer

Jill Tries to Climb IPO Hill

,

and

Kris Tuttle

March 7, 2017

. 2:16 PM

4 min read

Share on Twitter

Share on Facebook

Share on Pinterest

Share on LinkedIn

Share on WhatsApp

Share via Email

This post is for paying subscribers only

Subscribe

Already have an account?

Sign In

Related

Company Notes

Yesway is at Least a Maybe

,

and

Kris Tuttle

April 21, 2026

Spinoff

I Like Ice Cream

,

and

Kris Tuttle

February 19, 2026

Company Notes

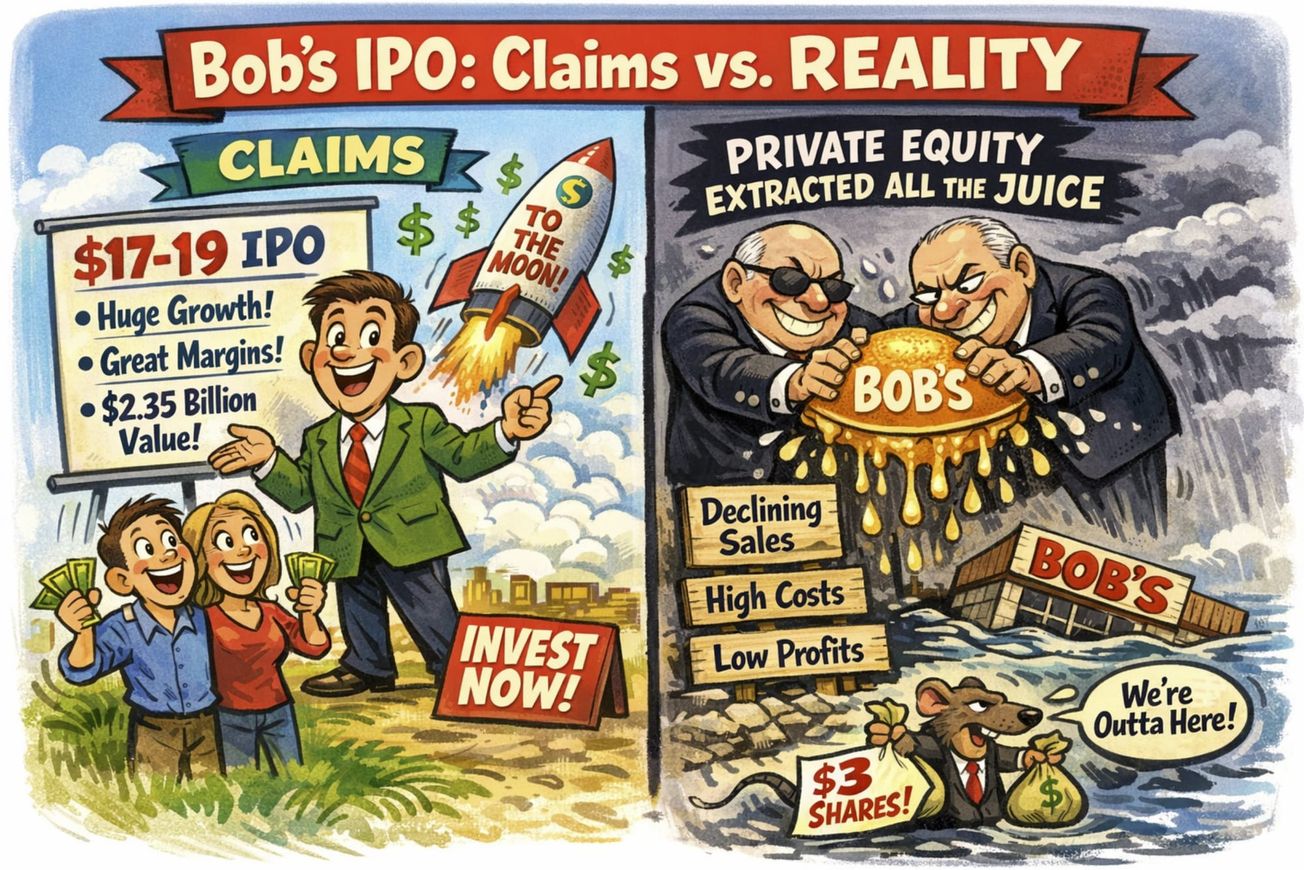

Bob's Very Overpriced Furniture

,

and

Kris Tuttle

February 2, 2026

Consumer

StubHub is Scrappy but...

,

and

Kris Tuttle

September 16, 2025

Latest

Decks

Vogenx (VOGX) IPO deck

,

and

Debarshi Ghosh

July 31, 2026

Decks

Braveheart Bio (BRVE) IPO deck

,

and

Debarshi Ghosh

July 31, 2026

Decks

Attovia Therapeutics (ATTO) IPO deck

,

and

Debarshi Ghosh

July 30, 2026

A Babe in a Bathtub

,

and

Kris Tuttle

July 28, 2026

{kind=link}